Signs the Creator Space is Maturing. Here is How.

Signs the Creator Space is Maturing. Here is How.

In a generation where emojis, memes and GIFs have taken precedence over phone calls and in-person meetings, the mass public have adopted more ‘relatable’ ways of communication. GIFs, memes, etc., often are packaged with nostalgia that instantly makes one smile, cringe or sad- by leveraging visual aid that our memories once felt a part of. Anything that happens in real life is no longer substantial, if not shared online (cannot blame Gen Z’ers as a lot of their life is virtual, they spend 74% of their time online).

It is here that creators, (defined by Li Jin, Founder Atelier Ventures, as those who have built up an audience on digital platforms) have etched the new-era of storytelling and built up an audience as large as megacities that are now ruling the roost. In India itself, the influencer market is estimated at $75-150 million a year, as compared to the global market of $1.75 billion (according to digital marketing agency AdLift) .

To make sense of key trends in India, we spoke to multiple creators, influencer management agencies, startups and investors. Here is what we found:

1) Creators emerging as D2C Brand Founders.

So far, consumer brands world over have been cashing in on Influencers/ Creators endorsing their products and until recently, there were thin lines of differentiation between brand placements and promotions and the creative liberties of Influencers.

However, that changed when American YouTuber Mr. Beast (Jimmy Donaldson) recently launched the MrBeast Burger chain along with restaurateur Robert Earl. It marked the advent of Creators launching their own D2C (Direct 2 Customer) brands and in this case sold over a million sandwiches in just two months.

“The key aspect of any new D2C brand is how it is distributed and builds brand value over a sustained period of time. Having a vast distribution solves for CAC (customer acquisition costs) and with community love, creators have a strong customer base that comes back for more,” says Viraj Sheth, Co-founder of Monk Entertainment, a Mumbai-based talent management and influencer marketing firm, currently managing at least 45 Creators.

Closer home, Mumbiker Nikhil (nicknamed YouTube ka Salman Khan) with 3.69 million YouTube subscribers has launched his own merchandise, LabelMN on Shopify.

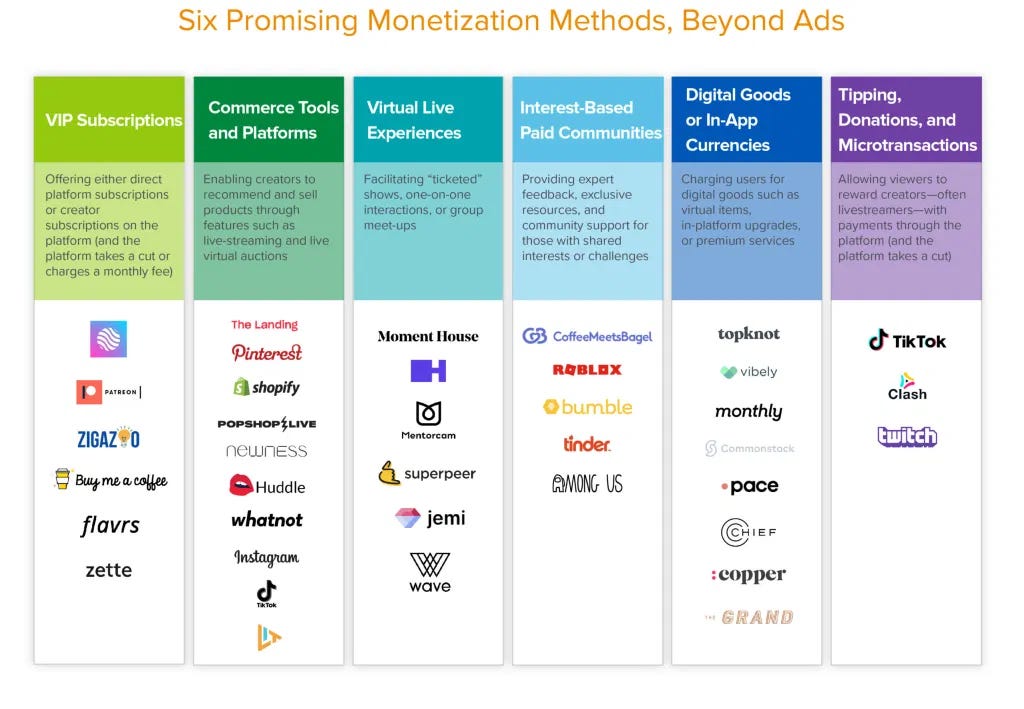

2. The various facets of Monetization.

Today, many social companies are experimenting with new monetization models, taking a page from China, the gaming industry, and early ad-adverse pioneers like Tinder, Spotify, and Venmo (Source a16z).

Saloni Srivastava, Founder of HustlePost Academy, has helped 2000+ creators start their own businesses and is an online course expert. She says, “I treat my business as my startup. My end-goal is to build a sustainable company.” Like Srivastava, many content creators are now starting their own courses.

Ranveer Allahbadia, one of the oldest creators on social media has been online for more than 6 years and has a 7 million followership. He has a six-module subscription-based course on Graphy on “Building a Social Media Umpire” as well.

Creators like Sejal Kumar are replacing celebs in brand endorsements and StyleMeUpWithSakshi, a body advocate/creator/model has her own co-branded range with L’Oreal.

That is not it, some of the big daddies in the creator space are also turning Angel Investors like Tanmay Bhat and Ranveer Allahbadia who have invested in Qoohoo, a platform that helps creators monetise their followers, and Ready Set Jet, an American beauty brand looking to India for expansion, respectively.

3. Going C2C.

According to Harsh Snehanshu, Founder Yourquote, a mobile app that allows creators to share short stories and text in 15+ languages, “Creator economy is where the creator and consumer are interacting directly and in India, it is still in its infancy. Two to three years down the line, we will have more Creators making money through the C2C (creator to consumer) model.”

YourQuote currently has 2.5 million writers on the platform and aims to cross 10 million by 2023 and 15 thousand creators have started making money directly from subscribers, by publishing books and paid stories.

Ankur Warikoo, Founder nearbuy.com, Mentor, Angel Investor and Public Speaker believes, “the next decade is going to see the rise of mega influencers/creators. In Fact my prediction is that this decade will see the world's first one-person unicorn emerge!

This will be spread across:

1. Mega creators (video, podcast, newsletters)

2. Mega teachers (how to guides, cohort based courses (CBCs), education) and

3. Mega Influencers (entertainment, beauty & wellness, self-help)”

He personally wants to create a million entrepreneurs in the next 10 years.

4. The growing Creator stack.

Creators are exploited by media platforms and some even have to pay the platform for their audience. Therefore creators are looking for more reliable ways to build their audience. Thus comes the need for a full stack platform that provides: Listing -> Discovery -> Growth -> Financing options to creators.

Kevin William David who is currently building Creatorstack, a platform to encourage more creators to take full control of their growth and become self-sufficient said, “What Shopify did for small businesses, Creatorstack does for creators (i.e.) helping creators have a closer connection with fans.” Content, Commerce, Culture and Community are important to a creator. There are many tools for each of them separately. He continues, “Creators should consider themselves as entrepreneurs and like any small business they need a ready business-in-a-box stack that brings all these tools together. We also have a creator fund where we invest in creators.”

Previously the journey of a creator was focussed on content, today is it broader and they are looking at themselves as unicorns, says Vimal Singh Rathore who is building Qoohoo, a platform empowering creator freedom, funded by Tanmay Bhat, Hugo Amsellem (investor in Creator Economy) and many others.

Others building tools for creators in India include: Cre Club (financial services for creators), nocolo.co (no code tool to build).

5. Regulation catching up.

Whether it is on Clubhouse or any other platform, regulation is still evolving. Earlier, brands used to push sponsored posts as organic content and to curb this, the Advertising Standards Council of India (a self-regulatory body) has come up with its own guidelines about disclosing brand partnerships. These guidelines are still a draft and will go live on March 31st, 2021.

“With creators directly monetising from their audience, there have to be guidelines where if the audience feels cheated, there should be a forum they can take this up to. With many platforms this still does not exist,” said Rahul Singh, Founder Winkl, a company that helps brands and advertisers run fully automated and data-driven influencer marketing campaigns.

“The ASCI has issued the guidelines at the right time when influencer marketing is hitting its peak. In my regional world of influencers, I have seen many people falsely promote brands before acquiring correct knowledge which will come to a standstill. Also, the audience will be able to distinguish between a branded and organic post promptly,” says Mohak Narang, Vlogger and content creator.

Although the ASCI is not a Government enforced regulatory authority, these directives come in as a breather for this fast-paced creator space.

The downside:

Creators are still platform dependent. They get locked out of their accounts. TikTok got banned in India, which has led to creators now creating their own content platforms. Sustained finances are still restricted to the cream of creators/ conversely, only the bigger influencers still wield most influence. This also means there is high pressure in image maintenance and churning out great content. This pressure is creating the next wave of demand and trends allowing micro-influencers to also dominate due to low barriers of entry, no frills set-up and a bunch of platforms to experiment with.

VCs are still not very active in this space (except a few - Li Jin) or creators themselves becoming investors.

Brands do not renew licenses or contracts in the long run. Neither do they (still) strategically use creators to co-create products or services.

Some emerging trends:

Bigger creators becoming more cult-like. Moving to OTT, spawning more amateurs, becoming bootstrapped Founders. Example: YouTuber and Blogger Prajakta Koli landed her first Netflix series and also got to interview Michelle Obama. More funds for creators like Atelier.

Platforms being more creator dependent. Example: Twitter Super Follow, Substack or even Clubhouse need adoption from the bigger folks to create mass engagement.

Clearer demarcation between (content) creators, passion economy and influencers.

Normalising subscriptions and fan funding. Built in features to ensure fans keep paying to continue to stay in touch with their idols. Example: YouTube superchat feature where fans pay a certain amount every month to their favourite YouTuber for BTS (behind-the-scenes), early looks etc. Obvious on Tanmay Bhat’s live streams.

Closer fan circles. Fans working with their favourite creators. Co-creating products. Much more highly engagement relationships.

Formation of a creator union and guidelines on how to work with creators.

This space is definitely heating up as reflected by the number of new platforms coming up, engagement and also rise in the number of creator-entrepreneurs. However, it is highly competitive and still only those with high audience engagement and followers will survive/ build the largest businesses. It is these large creators who can spawn many smaller creators/ amateurs and work with them/ fund them/ mentor them and continue to add value to this space. It definitely should go from a side-project kind of space to this is the ‘only-thing-i-do-and-excel-at’ (and make enough money) kind of space.

***